On Friday, March 10, 2023, the 12th-largest bank in the US was forced to close its doors, as the California state watchdog swooped in to take control of its assets. Silicon Valley Bank (SVB) had been a stalwart of the technology and startup scene for decades, providing banking services to some of the most innovative companies in the industry. Yet, in a dramatic few days, SVB started showing signs of stress before a stunning collapse left the bank’s customers with large clouds of uncertainty hanging over their financial future.

It wasn’t the only bank to collapse. A day before, Silvergate bank, a darling of the crypto sector, suffered the same fate when it entered receivership. Both Silvergate and Silicon Valley Bank serviced a tech-minded clientele that got hit particularly hard by the depressed state of the economy. A week later, Signature bank was shuttered by state authorities citing ‘systemic risk.’

Rising interest rates and rampant inflation has dried up the liquidity that funded the startups and future unicorns conducting business with these banks. Yet, the collapse of Silvergate and Signature banking collapse is closely related to the crypto crashes of 2022, while Silicon Valley Bank’s concerns are much more troubling.

In hindsight, it was obvious. Silvergate, the bank that reported a $1 billion loss for 2022, following a brutal series of crypto meltdowns, shut its doors on March 9th, a day before SVB. Silvergate bank relies heavily on the business it gets from the crypto industry, and counted failed exchange FTX amongst its clients. Just when it seemed that the knock-on effects from the FTX collapse were over, Silvergate bank proved that it was unable to recover from the wound it suffered during the crypto crash of 2022. While the company’s balance sheet continued to bleed, Federal agencies coordinated to steer banks away from crypto, warning of “liquidity risks to banking organizations”, from the sector.

Unlike Silvergate’s client FTX, whose balance sheet was tracked live on-chain after the exchange went down, we have scant information about Silvergate’s current financial position. To get an understanding of the state the bank was in, we can look at its latest financial reports at the end of 2022, which revealed massive losses for the year. A closer look at the financial report reveals that Silvergate has the funds to meet its obligations, at least it did at the end of last year. To be more precise, the bank had $10.3 billion worth of cash and securities to pay out $9.3 billion worth of deposits. The problem lies in the fact that the bank’s security portfolio was heavily invested in bonds, which have been hit hard by the interest rate hikes initiated by the Fed.

Meanwhile, Signature bank was forced to close by regulators citing ‘systemic risk.’ According to Barney Frank, a former congressman, and Signature Bank board member, Signature bank was shut down because “regulators wanted to send a very strong anti-crypto message.”

While the agencies were busy policing Silvergate bank, Signature bank and the entire crypto sector, the collapse of Silicon Valley Bank (SVB) came as a surprise to many. The collapse of SVB sent shockwaves through the banking sector, raising questions about the nature of banking and the risks associated with it. However, an astute macroeconomic analyst could have seen this coming from a mile away.

Over the last few months, the Federal Reserve has embarked on a sharp program of rate hikes, causing a bond crisis of its own making. To understand the impact of interest rate hikes on bonds, let’s take a look at what happens to a $100 bond that pays 2% interest, or $2. Currently, the Fed’s aggressive rate hikes have jacked interest rates up to 5%. With interest rates paid on Treasury bills, the safest investment out there, so high, why would anyone buy a bond that only yields 2%? Therefore, the price of the bond has to drop until it is effectively yielding the same as Treasury bonds, or even more. In our case, the bond price would have to drop to $40 so that the $2 interest paid, or coupon, is equal to the 5% rate given by the Fed. Clearly, a sharp increase in interest rates completely destroys the bond markets.

Unfortunately for Silicon Valley Bank and its peers, the macroeconomic climate forced them to hold a lot more bonds than they bargained for. The boom year of 2021 brought in a rush of deposits that needed to be parked somewhere. Regulators made it clear that bonds were the only game in town for banks looking to purchase securities, causing SVB and others to buy massive amounts of bonds with the cash influx they took in during the boom. The problem for SVB is that its bond portfolio consisted mostly of long-term bonds that were hit hardest by the rising interest rates. Had the bank purchased short-term bonds, they would not have locked in an interest rate much lower than the current rate available in the market.

While rising rates increased the amount of interest SVB had to pay its customers, its long-duration bonds remained pegged to lower interest rates. This resulted in a decrease in the bank’s net interest margin (NIM), the difference between the interest earned on loans and the interest paid on deposits. A decrease in NIM can be detrimental for banks because it directly affects their profitability. If the NIM is decreasing, banks earn less on their loans, which reduces their revenue. Additionally, a decreasing NIM means that banks have less money to cover their operating expenses, such as salaries, rent, and technology costs.

Additionally, SVB evaded scrutiny from the legislation meant to protect against such outcomes. Most US banks don’t comply fully with Basel II regulations, which makes them vulnerable to financial risks. Specifically, SVB was exempt from disclosing two key ratios used to determine the health of a bank:

Adding insult to injury, SVB’s own lax risk management compounded the effects of the bond market turning sour. The bank made use of a neat accounting trick to hide the fact that they were losing money. To understand the trick, we must first introduce two accounting concepts related to the ownership of securities. When a bank owns a security such as a bond, it has two ways of recording it on its balance sheet:

A cursory glance at SVB’s finances reveals $15 billion worth of losses on HTM securities that did not make it onto the company’s income statement. However, as in the case of Silvergate bank, SVB had to move securities from the HTM to the AFS pool in order to shore up its capital position. In addition, SVB failed to hedge against its interest rate risk at all. Once the market sensed blood, it wasn’t long before SVB’s collapse. Panicked VCs and startups started withdrawing money,

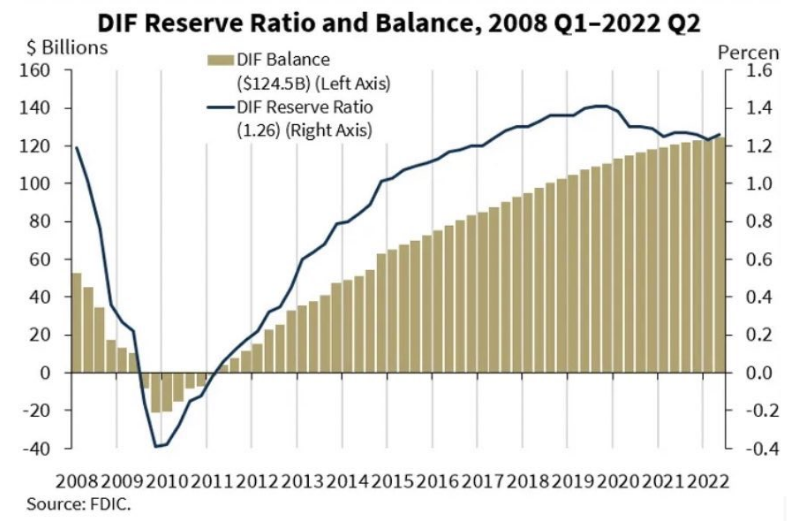

When the unfortunate collapse of a bank occurs, the US government agency responsible for stepping in is the Federal Deposit Insurance Corporation (FDIC). In the case of both Silvergate and SVB, the FDIC declared the failed banks ‘in receivership,’ which puts the banks totally under their control. Typically, the FDIC guarantees all insured deposits up to a $250,000 benchmark. Yet, that figure excludes high-net-worth individuals and businesses. In fact, the FDIC has enough assets to cover only 1.26% of all bank deposits in the US.

Thankfully for the anxious depositors, the government stepped in and ensured that all depositors would be made whole. It also stressed that this was not a bailout, since shareholders and management would lose everything.

Taking a step back from the chaos, we can ask ourselves a basic question. “Why do bank runs happen in the first place?” If I give the bank my money, why would I ever have trouble withdrawing it from the bank?

The fact is that at any given time, banks hold only a fraction of customer deposits in the form of cash or other liquid assets. Thanks to the invention of fractional reserve banking, banks can lend out or invest the majority of the funds they receive and earn interest on those loans, creating profits for the bank. When the market is doing well, banks have more than enough cash on hand to meet withdrawal requests. Yet, in times of distress, depositors rush to withdraw their money, overwhelming the bank’s capacity to pay out. In this case, banks have to sell off their assets in order to meet all the withdrawals that occur simultaneously.

In 2020, the Federal Reserve took the concept of fractional reserve banking to the extreme by introducing no-reserve banking. The move, taken in response to the COVID pandemic, meant banks were no longer required to maintain a minimum level of reserves to meet their customers’ demands. By eliminating reserve requirements, the Fed made the banking system more vulnerable to crisis, as banks were no longer required to hold a buffer of cash reserves to meet potential withdrawals.

When the world went indoors to flatten the curve of COVID, it caused a shock like no other to the economy. Frantic to avoid disaster, the Federal Reserve embarked on the most aggressive monetary expansion in history, cutting interest rates to near 0% and printing trillions of dollars in new money. Liquidity was now plentiful, and credit cheap, which led to a similarly aggressive spending boom and rapidly rising global markets. With an expanded pool of capital chasing a limited basket of goods and services, it was only a matter of time before inflation started spiraling out of control.

After initially dismissing inflation as ‘transitory,’ the Fed had no choice but to reverse course and start raising interest rates again. However, just as their rapid rate cuts led to inflation in the first place, raising rates by 4.25% in a single year contributed to the net interest margin facing banks like SVB. Although the Fed had planned to continue its rate hikes well into 2023, the sudden collapse of SVB and the distress faced by other banks could force the Fed to reconsider. However, the Fed could risk undoing its work to reduce inflation if it abandons rate hikes too early. Only time will tell which pill the Fed will take.

The first few months of 2023 have been a particularly harsh winter for crypto in the US, as regulators reacted zealously to FTX and other high-profile collapses. US agencies have taken aim at the crypto market, which has included shutting down Kraken’s staking-as-service, investigating Silvergate bank, and countless enforcement actions. The Fed, the FDIC, the SEC, and various agencies seem to want a barrier between banking and the crypto sector. At the same time, digital assets that are entirely compliant with US securities law continue to emerge on the scene.

These security tokens offer a way for investors to gain exposure to assets such as real estate or company shares using blockchain technology while ensuring compliance with securities regulations. By complying with securities regulations, security tokens may be able to bridge the gap between traditional finance and the crypto sector, offering investors a way to access the benefits of blockchain technology while maintaining regulatory compliance.

Overall, while the regulatory environment in the US may be uncertain at the moment, digital assets are likely here to stay. Digital asset legislation continues to evolve positively in countries like South Korea and Switzerland, causing a boom of innovation to emerge globally.

Monday the 13th of March will forever be a watershed moment for the digital asset markets. On the day when many distinguished bank stocks halted trading, Bitcoin, Ethereum and other cryptocurrencies rallied by over 10%. USDC, the stablecoin that lost its parity with the US dollar due to having funds stuck in SVB, recovered its peg and showed itself to be more resilient than the traditional banking sector.

Bitcoin, crypto, and digital assets are here to stay, whether certain powers that be like it or not. Digital assets in all their forms are shifting the world away from a reality where bank collapses are taken for granted. The future of finance as envisioned by ‘The INX Way’ consists of:

We can, and must, build a more resilient financial system that works for all.

Deputy CEO & Chief Operations Officer. Itai Avneri brings over 20 years of executive management experience to his role, and his commercial experience spans a number of technology and financial firms.